Solver-Based Execution

Solver-based execution is a trading architecture where users submit trade intents to a network of professional market makers (solvers) who compete to offer the best price. Unlike AMMs that rely on liquidity pools, or on-chain orderbooks that require matching engines, solvers source quotes from major centralized exchanges like Binance and Bybit, then settle trades fully on-chain. Carbon uses this model through the SYMMIO protocol, enabling CEX-depth liquidity on a decentralized exchange without custodial risk.

What Is Solver-Based Execution?

Solver-based execution is a trading model built on the concept of trade intents. Instead of placing an order directly into a liquidity pool or an orderbook, a trader signs and broadcasts an intent — a message specifying what they want to trade, at what terms, within what parameters.

Professional market makers called solvers receive this intent. Each solver evaluates whether they can fill it at a price that works for them, then submits a competing quote. The best quote wins. The trade settles on-chain.

The model is also referred to as intent-based trading or request-for-quote (RFQ) trading. The terms are roughly interchangeable, though intent-based trading is the broader category. The core insight is the same: instead of matching orders automatically through an algorithm, route them to professional market makers who compete to fill them at the best available price.

This is not a new idea. RFQ has been the dominant model in over-the-counter (OTC) derivatives trading in traditional finance for decades. When a fund wants to execute a large block of options or a currency pair, they send a request to multiple dealers and take the best quote. Solver-based DEXs bring that model on-chain.

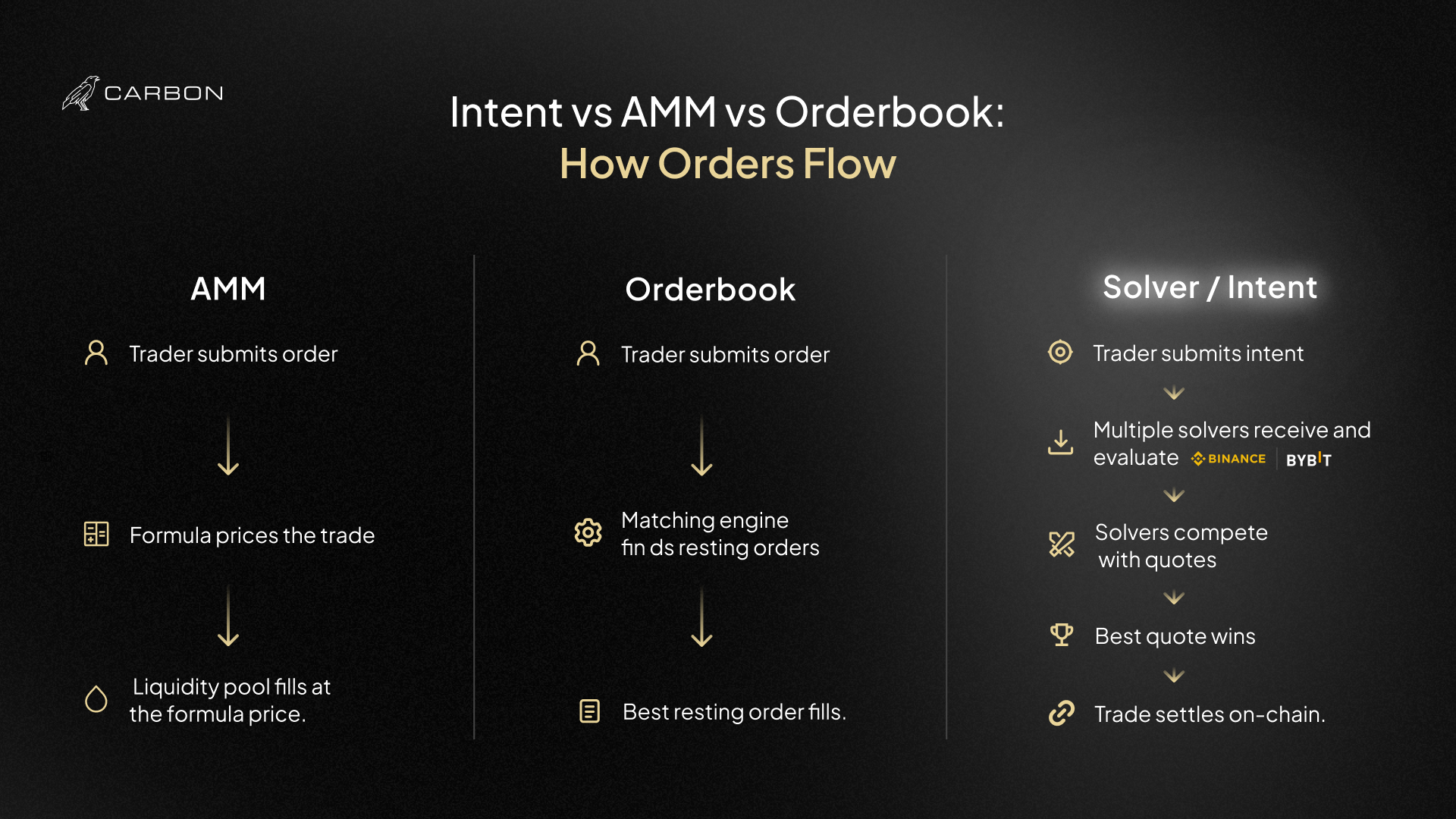

How It Differs From AMMs

Automated Market Makers (AMMs) price trades algorithmically based on the ratio of assets in a liquidity pool. The formula — most commonly x×y=k — determines what price you get. No market maker is involved. No competition occurs. The pool and the formula are the entire pricing mechanism.

This works for simple spot swaps on liquid pairs. It produces poor outcomes in derivatives contexts at scale.

Depth is bounded by pool capital. The deeper the pool, the less price impact. But LP capital is expensive — liquidity providers require meaningful returns to deploy it, and covering 550+ trading pairs with pool-based liquidity requires enormous capital commitments. Most pairs in an AMM-based perp DEX will have thin books.

LPs carry directional risk. When traders are consistently profitable — as happens during trending markets — LP pools absorb the losses. GMX’s GLP pool is the most studied example of this dynamic. The risk is real and limits how aggressively LPs can fund pools on volatile or less liquid assets.

AMMs don’t compete for your order. The formula gives you one price. In a solver model, multiple market makers compete, which creates the possibility of price improvement relative to any single static quote.

Composability for complex derivatives is limited. Bilateral positions, multi-leg strategies, and the specific collateral mechanics of a solver-based derivatives platform don’t map cleanly onto AMM architecture.

How It Differs From On-chain Orderbooks

On-chain orderbooks replicate the CEX model: market makers post resting bids and asks, takers fill against them, a matching engine pairs orders. The depth at any moment depends on how many market makers are actively quoting and how tight their spreads are.

When this works well, it’s excellent. Hyperliquid has demonstrated that a well-designed on-chain orderbook on a purpose-built chain can achieve genuine CEX-quality execution on major pairs.

The constraint is market maker behavior. Market makers are rational actors who widen spreads and reduce depth during high volatility — exactly when traders most need good execution. The time when liquidity matters most is when it’s hardest to get.

There is also a structural throughput challenge. Every order, cancel, and modification is an on-chain operation. High-frequency market making requires extremely fast finality and low fees, which pushes toward purpose-built infrastructure. This is why Hyperliquid built its own L1 and dYdX v4 migrated to Cosmos.

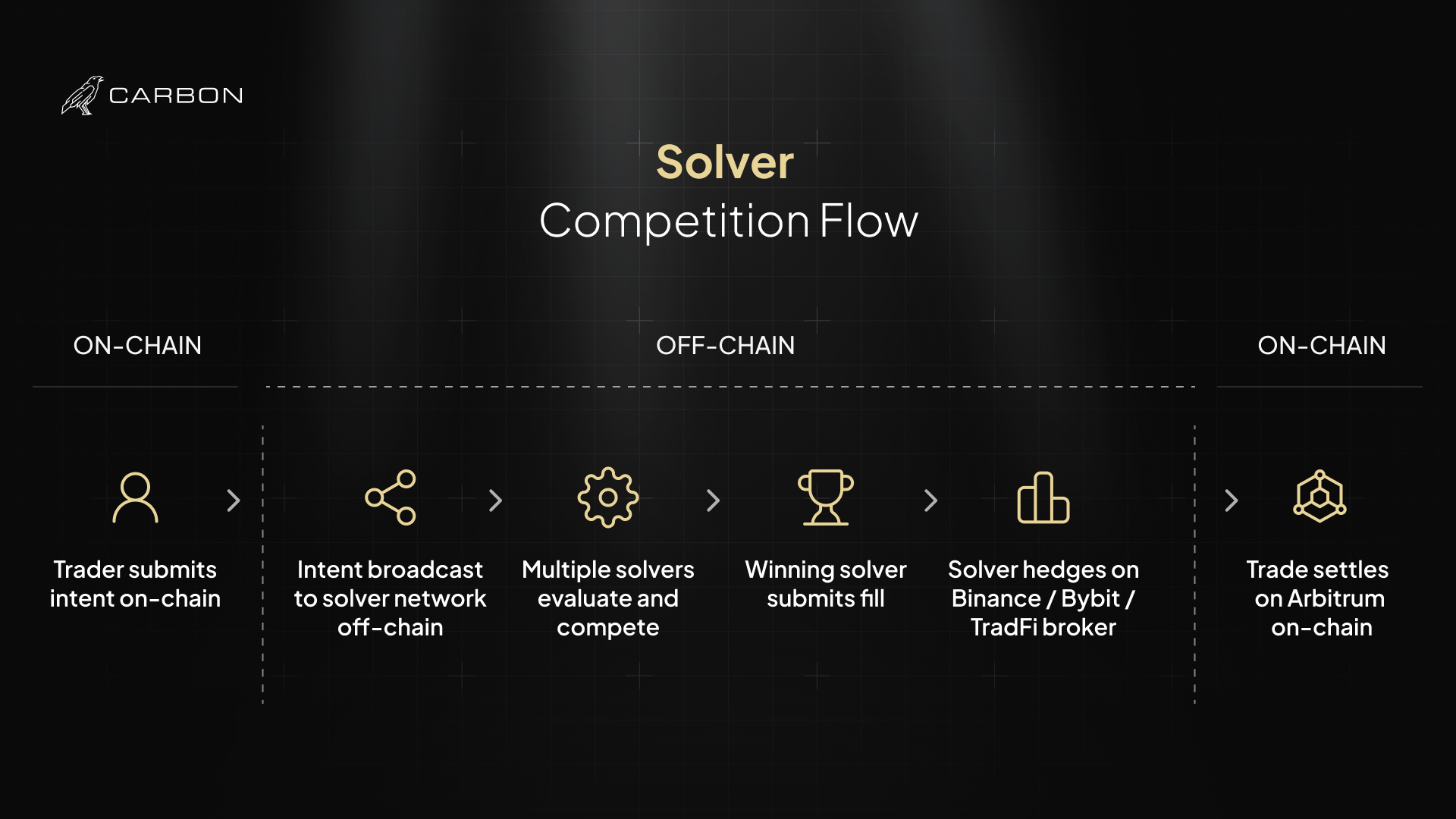

Solver-based execution sidesteps this problem by moving the price discovery and quote competition off-chain. Solvers receive intents and compete using their own off-chain systems. Only the final settlement touches the chain. The chain handles settlement, not the full order management lifecycle.

The Solver Competition Model

When a trader submits an intent on Carbon, the following sequence occurs.

The intent is broadcast to the Carbon solver network. Multiple professional market makers receive it simultaneously.

Each solver evaluates the intent. Solvers have real-time connections to Binance, Bybit, and other major exchanges. They check available liquidity, assess their own inventory and risk positions, and calculate what price they can offer while maintaining a viable hedge.

Solvers submit competing quotes. The auction is brief — milliseconds to a few seconds. The best available quote wins.

The winning solver commits to the fill. The trade is confirmed and settlement begins on-chain through the SYMMIO protocol. The solver simultaneously executes offsetting trades on their connected external venues to hedge their exposure.

The trader’s position is held on-chain. Despite the solver’s hedging happening off-chain, the trader’s margin, position size, and P&L are managed by smart contracts. The trader doesn’t interact with or know which solver filled their order. They receive the best available price.

This competition mechanism is what separates solver-based execution from alternatives. AMMs price with a formula. Orderbooks match against posted orders. Solver networks generate fresh competition on every single trade, sourced from wherever real-world liquidity is deepest.

How Solvers Source Liquidity

The critical question is: where does the actual depth come from?

For crypto perpetuals, Carbon’s solvers hedge on Binance, Bybit, OKX, and other major centralized exchanges. When a trader opens a 10 ETH long on Carbon, the solver filling that trade simultaneously opens an offsetting short on Binance or distributes across multiple venues. The solver’s net exposure is flat. Their profit is the spread between what they charged the trader and what the hedge cost.

For CFD markets on stocks, forex, and commodities, solvers are connected to institutional TradFi brokers with access to regulated equity markets, institutional FX venues, and commodity exchanges. A Tesla CFD is hedged through positions in actual Tesla stock, accessed through broker connections to NYSE liquidity.

This means Carbon’s liquidity depth is not limited by on-chain pool sizes or the willingness of on-chain market makers to quote. It is bounded by the depth of Binance’s order book, NYSE equity markets, and institutional FX venues — markets that collectively handle trillions in daily volume.

The practical result is that execution quality reflects real market conditions. If there is deep liquidity in the underlying market, Carbon users get tight spreads. If the underlying market is thin or volatile, that reality shows up in the quotes. This is honest liquidity: real depth, not manufactured pool depth that might evaporate under stress.

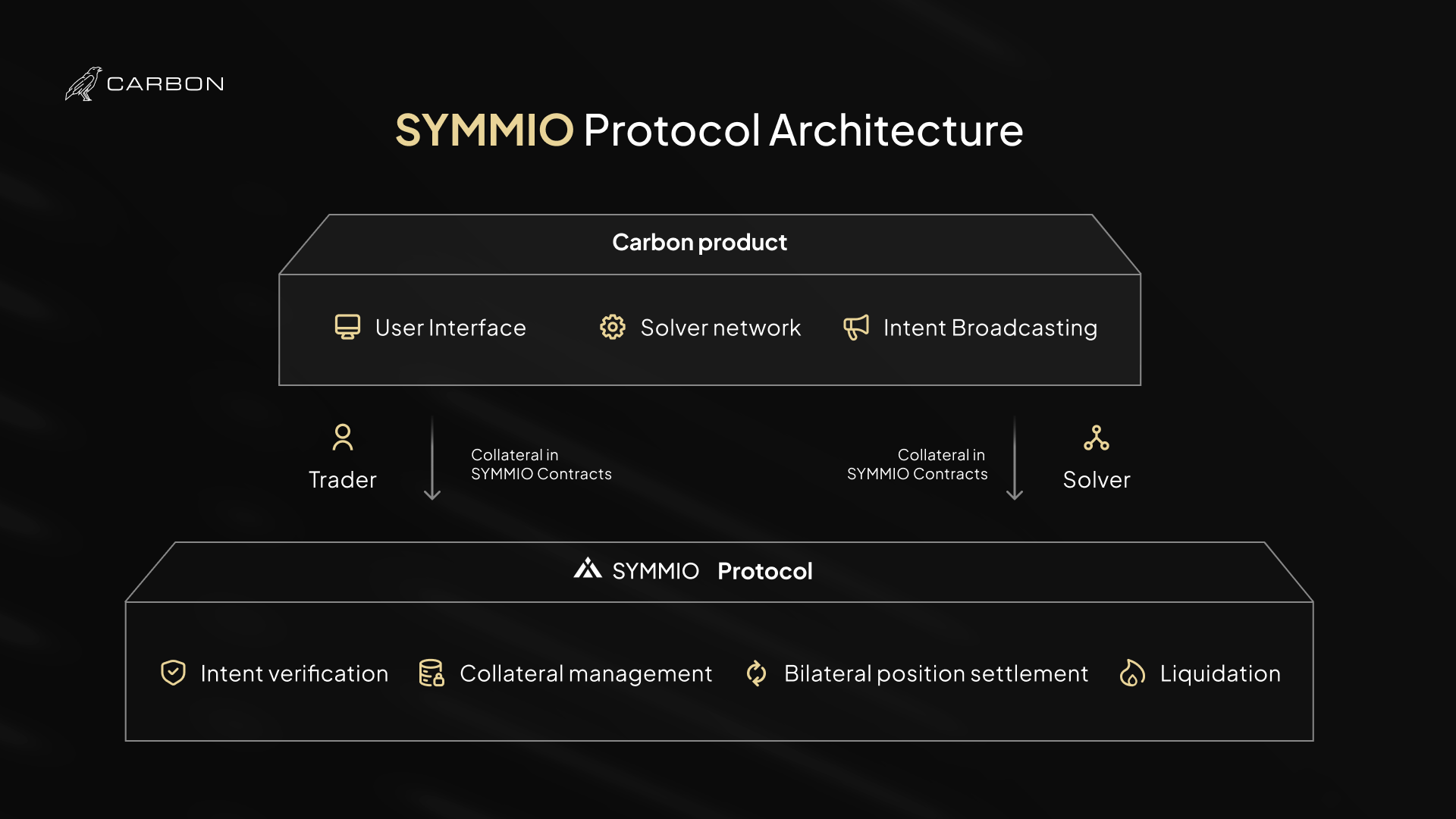

The SYMMIO Protocol

Carbon is built on SYMMIO, an open protocol for bilateral on-chain derivatives. SYMMIO provides the smart contract infrastructure that makes solver-based execution possible: verifying intents, managing solver collateral, enforcing settlement, and maintaining provably solvent bilateral positions.

Key properties of the SYMMIO architecture:

Provable solvency. Both the trader and the solver must post collateral into the protocol before a position opens. Positions are solvent by construction — the protocol doesn’t allow either party to open a position they cannot cover.

Atomic settlement. The fill and the settlement happen together. There is no settlement risk: either both sides settle, or neither does. You don’t have a situation where the solver defaults after your trade is open.

Transparent margin management. All margin calculations are on-chain and auditable. You can verify that your maintenance margin and liquidation threshold are computed correctly. There is no black box.

Non-custodial. Collateral is held in SYMMIO smart contracts, not by Carbon or any solver. Neither party can move the other’s collateral outside of the settlement process.

SYMMIO is not Carbon-specific. Other platforms are built on the same protocol. Carbon’s solver network, interface, and product layer are Carbon’s own implementation on top of this shared infrastructure.

Execution Quality

The proof of solver-based execution is in measurable outcomes: fill rates, execution speed, and slippage across trade sizes.

On well-capitalized solver networks, fill rates for standard trade sizes exceed 99%. Execution is near-instantaneous from the user perspective. Slippage on liquid pairs at moderate trade sizes is competitive with or better than major CEX execution.

The honest caveat is that execution quality depends on solver health. If solvers are not well-capitalized, if a solver goes offline, or if the hedging venues are temporarily inaccessible, execution quality degrades. Liveness risk — the risk that solvers are unavailable when you need to trade — is real in this model and must be managed through network redundancy and collateral requirements.

Carbon’s solver network currently includes Rasa Capital and additional solver partners. Network expansion is a continuous priority: more solvers means better competition, which means better pricing and higher liveness guarantee.

Why This Model Scales

Adding solvers to a solver network adds liquidity without adding smart contract complexity. Each new solver increases competition (better pricing), increases liveness (redundancy), and potentially adds new asset coverage if the solver has connections to different external venues.

Compare this to an LP pool model. Adding liquidity requires LPs to deposit capital into a specific pool. Adding a new trading pair requires creating a new pool or modifying existing ones. The system grows linearly with capital deployed.

In a solver model, adding a new trading pair is a routing question: can at least one solver in the network hedge that asset? If a solver has connections to commodity markets, Carbon can list gold. If a solver is connected to equity brokers, Carbon can list stocks. The protocol itself doesn’t need to change. The smart contracts don’t need to change.

This is why Carbon can offer 550+ crypto pairs and 200+ CFD markets from day one, and why the asset list can expand without fundamental architectural changes.

Trade-offs

Solver-based execution is not strictly better than all alternatives in every dimension. These are the real trade-offs, stated clearly.

Liveness dependency. The model requires active, well-capitalized solvers. An AMM is always available as long as the pool has funds. An orderbook executes against any resting limit order. If solvers are offline or unwilling to quote, trading halts. Mitigated through network redundancy, but not eliminated.

Settlement finality. On-chain settlement introduces finality delays relative to CEX execution. On Arbitrum, this is measured in seconds, not minutes. It is not zero.

Trust assumptions in solver behavior. While the protocol is non-custodial, traders trust that the winning solver will honor the quote and hedge appropriately. If a solver fills a trade but fails to hedge, the SYMMIO solvency mechanisms limit the damage, but a solver default event would be a degraded experience.

Composability constraints. Bilateral positions are harder to compose with other DeFi protocols than simple pool-based LP positions. This matters less for pure trading use cases but is relevant for structured products built on top of the platform.

These are known, manageable trade-offs, not hidden risks. The value exchange is: accept these constraints, get CEX-quality execution on a self-custodial, decentralized platform. For the traders Carbon targets, that trade-off is worth making.

Start Trading

Carbon’s solver-based execution is live for 550+ crypto perpetual pairs. CFD markets on stocks, forex, indices, and commodities are launching soon.